Offshore Market Report - Sept 2023

Of the 13,293 vessels and 3,749 barges Marcon tracked as of mid-September 2023, 2,933 are supply and tug supply boats, with 207 officially on the market for sale. 50.00% of foreign and 67.01% of U.S. flag supply / tug supply boats Marcon has officially listed for sale are direct from Owners. In addition to those for sale, Marcon has 86 straight supply and tug supply vessels listed for charter worldwide.

1,152 of the vessels tracked by Marcon as of mid-September 2023 are crew, fast supply & pilot boats with 148 officially on the market for sale, plus 52 boats are available for charter worldwide. 48.6% of the boats officially for sale are U.S. flag. 25 crew boats for sale worldwide were built within the last 10 years. 55 boats, or 37.16%, are 25 years of age or older. The oldest boat listed is a 40', 240BHP 1957 built and located U.S. West Coast. This vessel is counterbalanced by a 170.6' LOA foreign 2022 built crew boat in Southeast Asia.

Market Overview

Tug supply boats officially on the market for sale listed with Marcon in total is 66, 10 fewer than September 2022 and 68 fewer than September 2018. Composition now versus five years ago has changed with dropping 51 AHTSs in the 4,000BHP to 8,000BHP ranges. The largest change compared to last year was losing six in the over 12,000BHP category. September 2018, the average age of all AHTSs for sale was 15 years old, where U.S.-flag vessels averaged 29 years and foreign-flag AHTSs averaged 14 years. Today, the average age is 18 years old, with U.S.-flag AHTSs averaging 25 years and foreign-flag averaging 17 years old. At the time of this report, 14 tug supply boats officially for sale were either built within the last 10 years, including one newbuilding re-sale. 19.70%, or 13, of tug supply boats are 25 years of age, compared to five years ago, when 20.15% of AHTSs for sale were at least 25 years old; and one year ago, 10.67% were at least 25 years old. At September 2023, the oldest AHTS available from Marcon was a 1973-built, 191', 4,600BHP foreign flag AHTS located in Central America.

Tug supply boats officially on the market for sale listed with Marcon in total is 66, 10 fewer than September 2022 and 68 fewer than September 2018. Composition now versus five years ago has changed with dropping 51 AHTSs in the 4,000BHP to 8,000BHP ranges. The largest change compared to last year was losing six in the over 12,000BHP category. September 2018, the average age of all AHTSs for sale was 15 years old, where U.S.-flag vessels averaged 29 years and foreign-flag AHTSs averaged 14 years. Today, the average age is 18 years old, with U.S.-flag AHTSs averaging 25 years and foreign-flag averaging 17 years old. At the time of this report, 14 tug supply boats officially for sale were either built within the last 10 years, including one newbuilding re-sale. 19.70%, or 13, of tug supply boats are 25 years of age, compared to five years ago, when 20.15% of AHTSs for sale were at least 25 years old; and one year ago, 10.67% were at least 25 years old. At September 2023, the oldest AHTS available from Marcon was a 1973-built, 191', 4,600BHP foreign flag AHTS located in Central America.

At 141 platform supply vessels listed for sale mid-September 2023, we have 27 fewer PSVs listed for sale compared to one year ago and four less than listed five years ago. Looking at change in vessel size composition over the past year, the larger decreases were in the under 150' LOA (down 7); 180'-190' LOA (down 9); and 200'-220' LOA ranges (down 8). There was an almost complete offset between the 220'-240' and over 240' LOA ranges as the first increased by 10 while the latter decreased by 11. PSVs now being offered are slightly older than those offered back in September 2018 with the average age of all available for sale at 21 years old compared to 20 years old then. U.S.-flagged PSVs decreased from 22 years to 21 years, while foreign flagged increased from 16 to 20 years old. As of this report, Marcon officially has available 17 supply boats built within the last ten years, with no newbuilding resales listed. 35 PSVs, or 24.82%, are 25 years of age or older, with the oldest PSV listed built in 1971 - compared to one year ago when 31 PSVs (18.45%) were older than 25 years. Five years ago, 41 PSVs (28.47%) were older than 25 years, but 2 or 1.40% were newbuild resales.

At 141 platform supply vessels listed for sale mid-September 2023, we have 27 fewer PSVs listed for sale compared to one year ago and four less than listed five years ago. Looking at change in vessel size composition over the past year, the larger decreases were in the under 150' LOA (down 7); 180'-190' LOA (down 9); and 200'-220' LOA ranges (down 8). There was an almost complete offset between the 220'-240' and over 240' LOA ranges as the first increased by 10 while the latter decreased by 11. PSVs now being offered are slightly older than those offered back in September 2018 with the average age of all available for sale at 21 years old compared to 20 years old then. U.S.-flagged PSVs decreased from 22 years to 21 years, while foreign flagged increased from 16 to 20 years old. As of this report, Marcon officially has available 17 supply boats built within the last ten years, with no newbuilding resales listed. 35 PSVs, or 24.82%, are 25 years of age or older, with the oldest PSV listed built in 1971 - compared to one year ago when 31 PSVs (18.45%) were older than 25 years. Five years ago, 41 PSVs (28.47%) were older than 25 years, but 2 or 1.40% were newbuild resales.

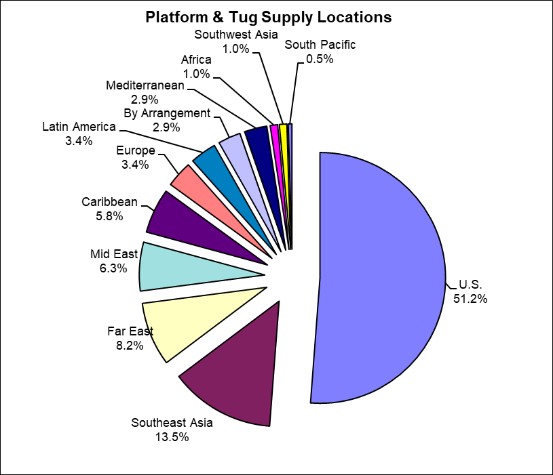

The dominant location for second-hand tonnage on the market September 2023 is the U.S. with 51.2% (up from 48.4% one year ago and 35.1% five years ago) followed by Southeast Asia with 13.5% (down from 13.9% one year ago and from 19.4% five years ago), Far East with 8.2% (compared to 11.5% last year and 11.8% in 2018), Mid-East with 6.3% (6.6% in 2022 and 9.7% in 2018), Caribbean 5.8% (3.7% in 2022 and 3.9% in 2018), Europe and Latin America with 3.4% each (compared to 3.3% and 2.9% one year ago and 3.9% and 2.2% five years ago, respectively) and Mediterranean 2.9% (up from 1.5% last year and 2.5% in 2018). Where location is unknown is 2.9%. The rest of the globe makes up the final 5.5% of locations. CAT is the principal main engine supplier to this sector powering 108 (54.9%) of the 207 supply & tug supply vessels listed for sale, followed by Cummins in 30 (14.6%), EMD and Wartsila with 13 each (6.3% each) and 11 with Bergen (5.4%). 30 (14.6%) units are powered by 13 other manufacturers. Compared to five years ago, the percentage of available for sale PSVs and AHTSs powered by CATs increased by 20.4 percentage points, while those powered by EMD dropped by 4.1 percentage points, Wartsila increased 1.0 percentage points and Cummins rose 0.6 percentage points.

Crew boats officially on the market now are down 56 and 63 from one year and five years ago, respectively. In terms of vessel size by LOA available compared to five years ago, we saw the most significant declines in crew boats of 40'-50', 100'-110', 110'-120' and over 130' LOA. As of this report, 16.89% of the crew boats available are less than 10 years old, down from the 26.47% and 23.22% reported one and five years ago, respectively. Conversely, 37.16% today compared to 28.92% last year and 38.39% five years ago are 25 years or older. Five years ago, the average age of all on the market through Marcon was 22 years, compared to 20 years one year ago but same as this report. Older U.S.-flagged vessels remain on the market, only decreasing slightly in age from 28 years in 2018 and 2022 to 27 years now. Foreign flagged crew boats' age fluctuated slightly over the past five years from 18 years five years ago down to 14 years old last year, back up to 16 years currently. However, these still trend over a decade younger than U.S. vessels.

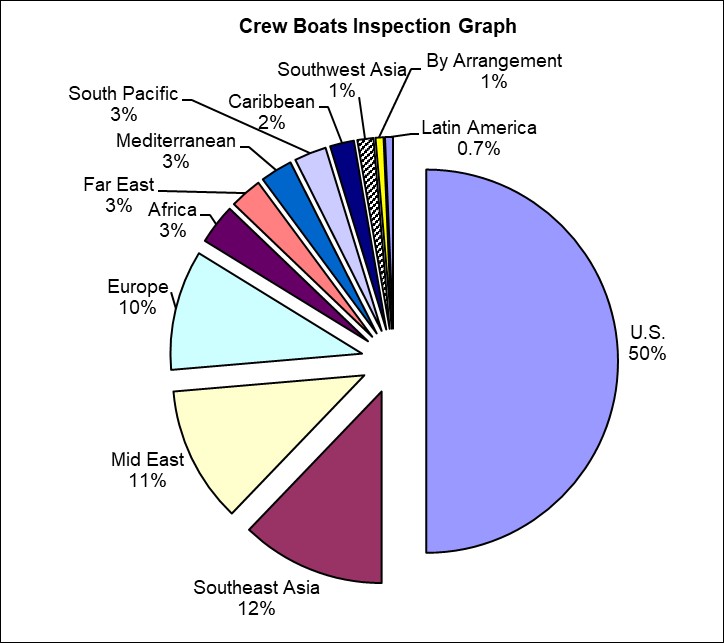

The dominant location for second-hand tonnage on the market September 2023 is the U.S. with 50% (up from 38.2% one year ago and 39.3% five years ago) followed by Southeast Asia with 12.2% (down from 15.2% one year ago and up from 11.8% five years ago), Mid East with 11.5% (compared to 11.3% last year and 8.5% September 2018 and Europe with 10.1% (versus 10.8% last year and 12.8% five years ago). Where location is unknown is 0.7%. The rest of the globe makes up the final 15.5% of locations. Of the crew, pilot boats and launches listed, the most popular engine is CAT in 60 of 145 boats where engines are given, followed by 33 Cummins, 28 GM/DD, six with MTU, MAN-B&W with five and 13 under other types, ranging from Baudouin to Yanmar. Compared to one and five years ago, as a percentage of vessels available for sale, there was a significant increase in those powered by CATs, offset by decreases in those powered by Cummins and GM/DDs.

Marcon Broker's CommentsGOM OSV Market: Current market conditions indicate that the summer season in the US Gulf for Plug & Abandonment (P&A) work is slowing down due to weather conditions - so the mini supply / DP1 vessel market should soften in the coming months. Rates remain high and availability is tight for bigger DP2 over 240' supply vessels working long term deepwater projects. It is expected that demand for deepwater drilling projects will continue to rise assuming oil prices remain around current levels, given current geo-political conditions.

Next year could see a big uptick in P&A work as the effects of the Cox Operating / Cox Oil LLC $560m bankruptcy moves through the system. Cox operated 600 wells in more than 60 fields. The company would purchase aging wells that had been abandoned by the larger independent and major oil companies. These wells are now being "transferred" back to their legacy owners to essentially either operate or shut down. These legacy owners now want these "assets" back off their books - so will likely press forward next year with aggressive P&A plans. If this expectation firms up - then this is going to create a large demand for P&A tonnage, especially crewboats and smaller OSVs.

Operating costs continue to rise across the board - from insurance to maintenance, parts through to incidentals like groceries. Labor shortages are a daily constant struggle in the market; as operators battle to retain their experienced seafarers.

This year has seen owners and operators jockeying to gain a foothold in North East Coast windfarm work that's beginning in earnest. Some GOM operators have sold operating and laid up vessels to specialist East Coast outfits - leading to vessel price increases and limited availability. Other owners have repositioned tonnage to this arena and have contracted directly with the wind farm operators.

The Bureau of Ocean Energy Management held its first ever offshore wind lease sale in the Gulf of Mexico but it failed to attract much interest with just one of the three available leases provisionally awarded to German developer RWE, and only two other bidders.

Several factors may have put the brakes on potential developer interest, including gulf winds being slower than other coastal areas, requiring the use of specific turbines. Frequent hurricanes are likely to raise costs as well. Also, construction costs for wind farms on the East Coast have soared due to inflation and supply issue constraints, so developers see less potential for returns. Requests by the major contractors for altering contract agreements with regulatory agencies in the US Northeast has thus far fallen on deaf ears. New York just recently completely rejected the pleas from companies for higher utility rates to compensate for the continuous rise in costs. This could contribute to a slow down on the overall success of efforts declared by the US Government related to its overall goal of 80% renewable energy generation in the USA by 2030, The offshore wind generated energy portion represents roughly 30 gigawatts of online production by 2030. In June 2023 this estimate was scaled back to 23.1 gigawatts, and after New York issued its rejection of the rate increase requests, a major research analyst, Atin Jain, senior wind analyst at BNEF, estimated that the US capacity may only reach a total of 16.4 gigawatts by the end of this decade, referring to the 30 gigawatts production effort as a 'pipe dream'. In some instances, companies have stated that they need to reassess their interest in new fields. Others have paid multi-million dollar fines to exit agreements with state regulatory agencies, and terminate contracts rather than walk into an arena of continually rising costs in the current environment.

Overseas OSV Market: The biggest news this cycle was Vroon agreeing to sell 30 offshore vessels and two management offices to Britoil Offshore Services, essentially doubling the Britoil fleet with the stroke of a pen. This followed on a four vessel deal with Golden Energy buying Vroon's "VOS Pacer", "VOS Passion", "VOS Paradise" and "VOS Partner" for US $94m.

Commercial Marine Brokers since 1981