Tug Market Report - May 2023

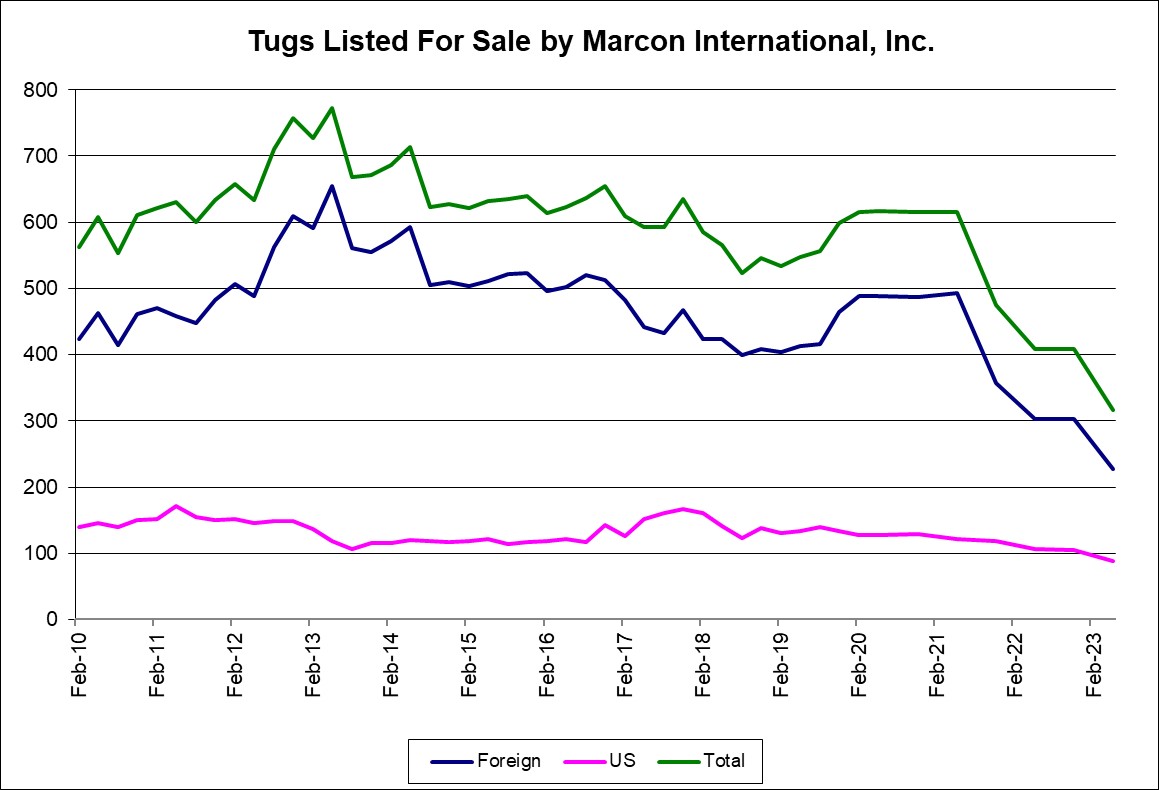

Of the 13,322 vessels and 3,757 barges that Marcon tracked as of May 2023, 5,184 are tugs with 316 officially on the market for sale worldwide, down 249 or 44.07% from one year ago, May 2022, and down 93 or 22.74% from May 2018. 95.51% of U.S. and 36.12% of foreign tugboats for sale are direct from Owners. 52 or 16.46% of the tugs worldwide, primarily foreign flagged, were built within the last 10 years, are newbuilding re-sales or currently under construction - compared to 19.80% one year ago and 35.04% five years ago. 53 (16.77%) are over 50 years of age, with five of those over 75 years old. Eight have no age listed. The oldest tug Marcon currently has listed is a 1940 built 122' LOA, 1,950BHP single screw tug located on the U.S. Great Lakes. This "old lady" is balanced by two twin screw tug newbuild resales for delivery in the U.S. in 2023 and 2024.

Marcon's Market Comments

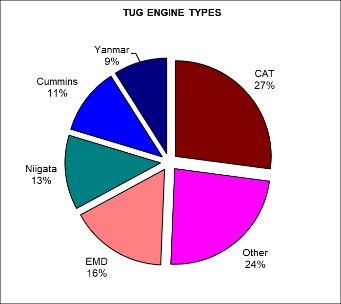

The majority of tugs Marcon tracks for sale as of this report are in the US with 89 tugs officially on the market (vs. 106 one year ago), followed by 59 in Southeast Asia (71), 34 in the Far East (52), 34 in Europe (53), 20 each in Latin America (29) and in the Mediterranean (33), 13 in the South Pacific (17), 9 each in the Caribbean (11) and in the Mid East (15), 7 where location unstated (10), 6 in Canada (7) and 2 each in Africa (5) and Southwest Asia (0). Where machinery is known, CAT diesels power 84 or 27% of the tugs listed for sale. This is followed by 51 vessels with EMDs, 39 Niigata, 35 Cummins, 28 Yanmar and 8 with Mitsubishi. 65 tugs are powered by other machinery from Akasaka to Wartsila with one Fairbanks Morse tug on the market.

The majority of tugs Marcon tracks for sale as of this report are in the US with 89 tugs officially on the market (vs. 106 one year ago), followed by 59 in Southeast Asia (71), 34 in the Far East (52), 34 in Europe (53), 20 each in Latin America (29) and in the Mediterranean (33), 13 in the South Pacific (17), 9 each in the Caribbean (11) and in the Mid East (15), 7 where location unstated (10), 6 in Canada (7) and 2 each in Africa (5) and Southwest Asia (0). Where machinery is known, CAT diesels power 84 or 27% of the tugs listed for sale. This is followed by 51 vessels with EMDs, 39 Niigata, 35 Cummins, 28 Yanmar and 8 with Mitsubishi. 65 tugs are powered by other machinery from Akasaka to Wartsila with one Fairbanks Morse tug on the market.

Five years ago, 35.04% of tugs for sale worldwide, primarily foreign flag, were built within the previous 10 years compared to 16.46% today. Then 11.86% of the tugs on the market were 50+ years old compared to 16.77% today. At that time, Marcon had five tugs older than 75 years same as today. The average age of all tugs that Marcon has for sale worldwide today is 30 years, with 1993 average build date, compared to 26 years, 1992 average built, in May 2018. The U.S. had the largest selection of tugs listed in 2018 with 141 available (25.0%), followed by 116 in Southeast Asia (20.5%), 65 in the Mid East (11.5%), 53 in Far East (9.4%), 49 in Europe (8.7%), Mediterranean 44 (7.8%), 34 in Latin America (6.0%), 18 in the Caribbean (3.2%), 15 Africa (2.7%), 11 in the South Pacific (1.9%), 10 Canada (1.8%), 7 where location is unknown (1.2%) and 2 in Southwest Asia (0.4%).

Five years ago, 35.04% of tugs for sale worldwide, primarily foreign flag, were built within the previous 10 years compared to 16.46% today. Then 11.86% of the tugs on the market were 50+ years old compared to 16.77% today. At that time, Marcon had five tugs older than 75 years same as today. The average age of all tugs that Marcon has for sale worldwide today is 30 years, with 1993 average build date, compared to 26 years, 1992 average built, in May 2018. The U.S. had the largest selection of tugs listed in 2018 with 141 available (25.0%), followed by 116 in Southeast Asia (20.5%), 65 in the Mid East (11.5%), 53 in Far East (9.4%), 49 in Europe (8.7%), Mediterranean 44 (7.8%), 34 in Latin America (6.0%), 18 in the Caribbean (3.2%), 15 Africa (2.7%), 11 in the South Pacific (1.9%), 10 Canada (1.8%), 7 where location is unknown (1.2%) and 2 in Southwest Asia (0.4%).

Looking at tugs for sale worldwide, conventional twin screw tugs lead with 196 (62.0%) available, followed by 80 azimuthing (25.3%), 27 single-screw (8.5%), seven Voith Schneider tractors (2.2%) and six triple screw (1.9%). This is fairly comparable to five years ago when 12.4% of the 565 tugs for sale were single screw, 60.7% twin screw, 23.2% azimuthing, 3.0% VS tractor and 0.7% triple screw tugs. Bearing in mind that we are focusing on those available for sale, it seems that for the past five years, azimuthing and conventional twin screw tugs have maintained steady positions in the market. Single screw tugs are mostly relegated to nearly zero commercial work, except in certain specific cases. Available for sale units have dropped considerably with many of those being scrapped due to age and condition. It is noted that in May 2023, Sea-Web reported 2,242 tugs worldwide scuttled, broken up or to be broken up world-wide. This is up 5.06% from May 2022's 2,134. Scrapped vessels increased 34.38% between May 2021 and May 2022, after averaging just over 2% from 2018 to 2019 and then 2019 to 2020. With the decrease in rate of scrapping, it seems that many companies have finished a concentrated effort to scrap its excess tonnage during the worst of the economic fallout of the pandemic. In certain areas of the market, we have seen an increase in demand for tugs and barges, with there being a shortage of units with desired specifications.

Marcon's database shows 93 fewer tugs officially for sale than five years ago in May 2018 with largest shifts in the lower horsepower categories. There are 23 fewer tugs are today listed in the 2-3,000HP range with average age increasing from 30 to 31 years. The 3-4,000HP range lost 22 tugs while their average age increased from 25 to 30 years. Below 1,000HP and the 1-2,000HP range each lost 13 tugs while average age increased six to eight years, respectively. The 4-5,000HP range decreased by 10 tugs with average age rising from 17 to 24 years. There were minor changes in the higher horsepower ranges as far as number available for sale and average age. In summary, we saw a 22.74% drop in listings with a four year increase in overall average age.

Marcon has closed 17 sales to date in 2023 with several additional sales pending. These sales included seven twin screw tugs ranging between 1,340BHP and 7,200BHP. Activity in the US tug market remains brisk with numerous tugs changing hands during the past quarter of 2023. Marcon has been involved in the domestic US market selling a US Flag 136' LOA 1978 McDermott SY built 5,750BHP tug from US West Coast Owners in the past month, as well as a US Flag 1,300BHP tug in Alaska and a Tier 3, 2,200BHP US Flag tug from the US Gulf to new Owners for employment in US Northeast wind farm support work. We have several offerings remaining in the US Market, including a 4,400BHP Twin Screw Ocean Tug which has just completed her 5 year dry-docking for ABS and USCG, and is ready to go with full refurbishment also completed. We also have a few smaller construction / dredge support tugs which can be developed, but we are finding it difficult to move tonnage into the expected high demand of the California dredge and marine construction markets at this time. This is mainly due to CARB (California Air Resource Board) requirements. The current CARB requirements appear to insist any and all newly imported vessels into the California market will now require Tier 4 main engines to enter that potentially lucrative market. Tier 2 is being phased out at the end of 2023, but instead of allowing Tier 3 tonnage to be brought in, CARB has declared that all new imports into the market shall be Tier 4 (which was not technically required until phasing out of the Tier 3 at the end of 2027). This has stymied many acquisition possibilities for owners and operators looking to continue their service in the Golden State, and may portend a day of reckoning when there are not enough acceptably tiered tugs to service the demand in that region.

Commercial Marine Brokers since 1981