Offshore Market Report - Sept 2022

Of the 13,439 vessels and 3,731 barges Marcon tracked as of mid-September 2022, 2,945 are supply and tug supply boats, with 244 officially on the market for sale. 67.65% of foreign and 75.93% of U.S. flag supply / tug supply boats Marcon has officially listed for sale are directly from Owners. In addition to those for sale, Marcon has 98 straight supply and tug supply vessels listed for charter worldwide, but there are many more in today's market idle and hungry for employment.

1,155 of the vessels tracked by Marcon as of mid-September 2022 are crew, fast supply & pilot boats with 204 officially on the market for sale, plus 32 boats are available for charter worldwide. 37.3% of the boats officially for sale are U.S. flag. 54 crew boats for sale worldwide were built within the last 10 years. 59 boats, or 28.92%, are 25 years of age or older. The oldest boat listed is a 40', 240BHP 1957 built and located U.S. West Coast. This vessel is counterbalanced by a 170.6' LOA foreign 2022 built crew boat in Southeast Asia.

Market Overview

Tug supply boats officially on the market for sale listed with Marcon in total is 76, 65 fewer than one year ago, September 2021 and 81 fewer than five years ago, August 2017. Composition in the last year has changed with the biggest shifts being 13 fewer 5-6,000HP, ten less 12,000-plus HP, eight less 7-8,000HP, seven each fewer 4-5,000HP and 8-9,000HP, six each less 6-7,000HP and 10-12,000HP and five fewer 3-4,000 HP AHTSs offered. August 2017, the average age of all AHTSs for sale was 14 years old, where U.S.-flag vessels averaged 25 years and foreign-flag AHTSs averaged 14 years. Today, the average age is 15 years old, with U.S.-flag AHTSs averaging 23 years and foreign-flag averaging 13 years old. At the time of this report, 24 tug supply boats (32.00%) officially for sale were either built within the last 10 years or are newbuilding re-sales. Only 10.67% of tug supply boats are at least 25 years of age, compared to five years ago, when 19.75% of AHTSs for sale were at least 25 years old and 9.93% one year ago, reflecting the purging of older units from the fleets over the past five years. At September 2022, the oldest AHTS available from Marcon was built in 1974.

Tug supply boats officially on the market for sale listed with Marcon in total is 76, 65 fewer than one year ago, September 2021 and 81 fewer than five years ago, August 2017. Composition in the last year has changed with the biggest shifts being 13 fewer 5-6,000HP, ten less 12,000-plus HP, eight less 7-8,000HP, seven each fewer 4-5,000HP and 8-9,000HP, six each less 6-7,000HP and 10-12,000HP and five fewer 3-4,000 HP AHTSs offered. August 2017, the average age of all AHTSs for sale was 14 years old, where U.S.-flag vessels averaged 25 years and foreign-flag AHTSs averaged 14 years. Today, the average age is 15 years old, with U.S.-flag AHTSs averaging 23 years and foreign-flag averaging 13 years old. At the time of this report, 24 tug supply boats (32.00%) officially for sale were either built within the last 10 years or are newbuilding re-sales. Only 10.67% of tug supply boats are at least 25 years of age, compared to five years ago, when 19.75% of AHTSs for sale were at least 25 years old and 9.93% one year ago, reflecting the purging of older units from the fleets over the past five years. At September 2022, the oldest AHTS available from Marcon was built in 1974.

Compared to one year ago, we have 33 fewer PSVs listed for sale. The greatest changes in the vessel size composition since September 2021 are 11 fewer over 240' LOA, seven less 150'-160', four fewer 180'-190' and four more 200'-220' LOA PSVs presently on the market. On the other hand, we have 24 more PSVs listed for sale now than we did August 2017, with 21 more 220'-240' LOA and nine more over 240' LOA. Similar to anchor handling tug supply boats, PSVs now being offered are closely the same age as those offered back in August 2017 with the average age of all available for sale 19 years of age. U.S.-flagged PSVs remained at 21 years, while foreign flagged increased from 16 to 17 years old. As of this report, Marcon officially has available 29 supply boats (17.26%) built within the last ten years, with zero newbuildings listed. 31 PSVs, or 18.45%, are 25 years of age or older, with the oldest PSV listed built in 1971 - compared to one year ago when 39 PSVs (17.89%) were older than 25 years and 40 (18.35%) were less than ten years with two newbuilds. Five years ago, 41 PSVs (28.47%) were older than 25 years, 44 (30.56%) were built within ten years with 9 or 6.25% newbuilds.

Compared to one year ago, we have 33 fewer PSVs listed for sale. The greatest changes in the vessel size composition since September 2021 are 11 fewer over 240' LOA, seven less 150'-160', four fewer 180'-190' and four more 200'-220' LOA PSVs presently on the market. On the other hand, we have 24 more PSVs listed for sale now than we did August 2017, with 21 more 220'-240' LOA and nine more over 240' LOA. Similar to anchor handling tug supply boats, PSVs now being offered are closely the same age as those offered back in August 2017 with the average age of all available for sale 19 years of age. U.S.-flagged PSVs remained at 21 years, while foreign flagged increased from 16 to 17 years old. As of this report, Marcon officially has available 29 supply boats (17.26%) built within the last ten years, with zero newbuildings listed. 31 PSVs, or 18.45%, are 25 years of age or older, with the oldest PSV listed built in 1971 - compared to one year ago when 39 PSVs (17.89%) were older than 25 years and 40 (18.35%) were less than ten years with two newbuilds. Five years ago, 41 PSVs (28.47%) were older than 25 years, 44 (30.56%) were built within ten years with 9 or 6.25% newbuilds.

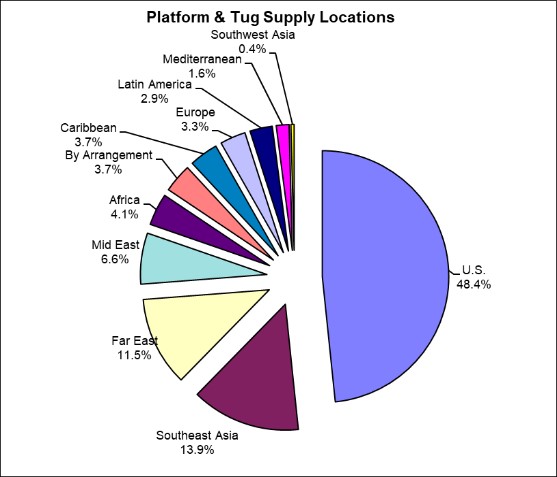

The dominant location for second-hand tonnage on the market September 2022 is the U.S. with 48.4% (up from 38.7% one year ago and 29.6% five years ago) followed by Southeast Asia with 13.9% (up from 18.1% one year ago but down from 24.9% five years ago), Far East with 11.5% (compared to 9.5% last year and 11.3% in 2017), Mid-East with 6.6% (8.6% in 2021 and 9.6% in 2017), Africa 4.1% (down from 6.4% last year and 6.3% in 2017) and Caribbean with 3.7% (compared to 4.2% last year and 3.3% five years ago). Where location is unknown is 3.7%. The rest of the globe makes up the final 8.1% of locations. CAT is the principal main engine supplier to this sector powering 128 (52.9%) of the supply & tug supply vessels listed for sale, followed by Cummins in 35 (14.5%), 17 (7.0%) each with Niigata, 17 (5.8%) with Bergen and 12 with EMD. 36 (14.9%) units are powered by various other manufacturers. Compared to five years ago, the percentage of available for sale PSVs and AHTSs powered by CATs increased by 12.2 percentage points, while those powered by Wartsila dropped by 10.8 percentage points, EMDs decreased 7.1 percentage points and Niigata fell 2.1 percentage points.

September 2022's number of crew boats officially on the market for sale by Marcon at 204 is down 24 from one year ago in September 2021 and up 21 from five years ago in August 2017. Over the last year, composition of LOA ranges has changed with the biggest shifts being 14 fewer 40'-50' LOA, six more over 130' LOA and five fewer each 60'-70' and 110'-120' LOA crew boats offered. As of this report, 26.47% of the crew boats available are less than 10 years old, up from the 27.63% reported one year ago but down from the 31.00% reported five years ago. Comparatively, 28.92% today versus 28.07% last year and 41.05% five years ago are 25 years or older. In looking at overall fleet age and then by U.S.-flagged versus foreign flagged , we can see slight changes in ages with those available today slightly younger than those offered five years ago. Five years ago, the average age of all on the market through Marcon was 21 years, compared to 21 years one year ago and 20 years as of this report. Older U.S.-flagged vessels remain on the market, decreasing from 32 years in 2017 to 29 years in 2021 and then to 28 now. Foreign flagged crew boats' age remained fairly steady at 16 years August 2017 and 15 years September 2021 compared to 14 years today, but are still half the age of U.S. vessels.

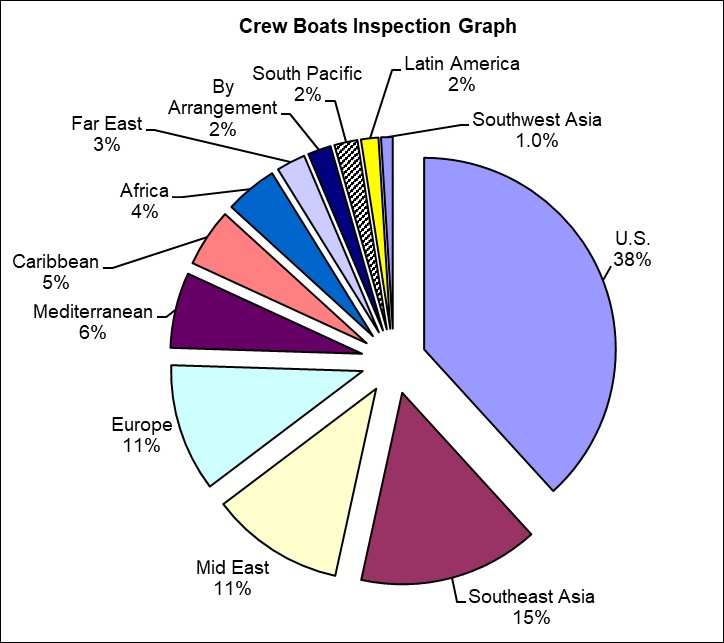

The dominant location for second-hand tonnage on the market September 2022 is the U.S. with 38.2% (down from 39.9% one year ago but up from 37.3% five years ago) followed by Southeast Asia with 15.2% (down from 15.8% one year ago and from 18.2% five years ago), Mid East with 11.3% (compared to 11.0% last year and 10.9% August 2017, Europe with 10.8% (versus 10.1% last year and 11.4% August 2017), and the Mediterranean with 6.4% (down from 7.0% last year and 4.1% five years ago). Where location is unknown is 2.0%. The rest of the globe makes up the final 16.1% of locations. Of the crew, pilot boats and launches listed, the most popular engine is CAT in 71 of 202 boats where engines are given, followed by 55 Cummins, 34 GM/DD, MAN-B&W and MTU in 10 each, 6 with Iveco, 4 with Volvo/Volvo Penta and 12 under other types, ranging from Baudouin to Yanmar. Compared to one and five years ago, as a percentage of vessels available for sale, there was a significant increase in those powered by CATs and MAN/MAN-B&Ws, offset by decreases in those powered by Cummins and GM/DDs.

The pandemic severely stalled sales activity from the second quarter of 2020 through the end of 2021. In 2021, we completed ten sales, primarily under "best offer" conditions and one charter. As of end of third quarter 2022, Marcon has seen more activity with thirteen sales completed and several others in process. In 2021, one sale was at sellers' asking price, while the remaining were heavily negotiated. To date in 2022, we have seen sellers' pricing adjusting to what the market is bearing for vessels of their age and condition or at just above scrap levels in order to get the vessel sold. Of our sales to date in 2022, nine sales were US to US parties, one was US to Canadian buyer and three were between foreign parties into Africa and Europe. In 2021, five of our nine sales were US seller to US buyer, one was US seller to foreign buyer, one was foreign to US buyer and two were foreign to foreign sales. Vessels were sold into the Caribbean and Southeast Asia.

Marcon Broker's CommentsThe offshore oilfield market has seen a marked improvement since our last market report in April 2022. Demand has been rising in the US and in international waters, and rates have been doubling and even tripling in certain segments, with related sale prices moving up accordingly. In some instances, vessels that could be purchased for a very sharp reduction over the past several years, have been removed from the market and placed back into employment, and sale prices are doubling and tripling in line with the demand. Very large (260' LOA and up) DP2 OSVs in the US Gulf have seen very strong demand and there are very few, if any, units to be considered for any would be Buyers. With increased oil prices, and expected increasing demand, many regions are starting to renew their efforts at increased exploration and extraction. Petrobras in Brazil is a case in point with a recent announcement to source another 20 vessels to support its expansion intentions.

The offshore wind market is also helping to strengthen overall demand for these typically oil exploitation related support vessels. There have been several sales in the international market where the vessel was sold to new Owners supporting offshore wind farm development. We would expect to see this trend continue, as newbuild costs for all classes of vessels continue to climb due to strong inflationary pressures that have been in effect for the past 12 months. Continued supply chain issues will tend to contribute to delayed newbuilding deliveries for the specialized assets moving into the offshore wind market, and existing tonnage will need to take up some of the slack in the meantime to meet the increasing demand in that offshore segment of the market.

Commercial Marine Brokers since 1981