Tug Market Report - Nov 2022

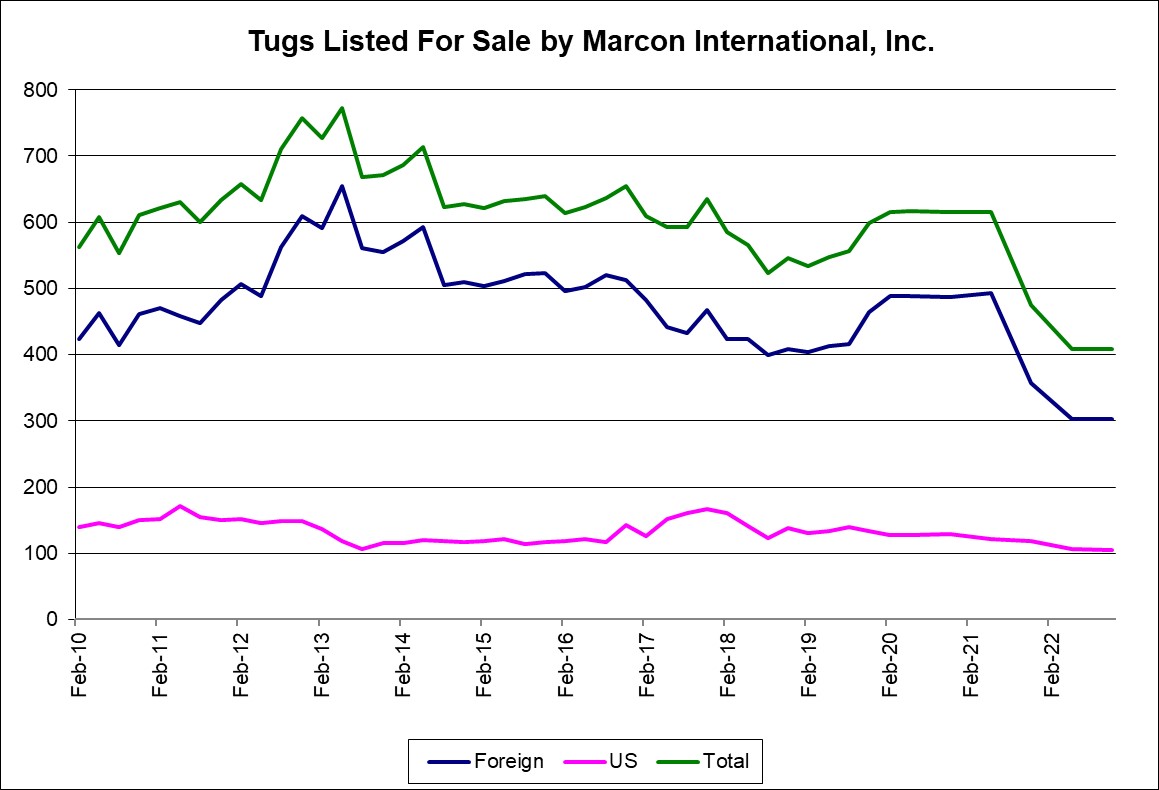

Of the 13,426 vessels and 3,742 barges that Marcon tracked as of November 2022, 5,199 are tugs with 408 officially on the market for sale worldwide, down 67 or 14.11% from one year ago, November 2021, and down 227 or 35.75% from November 2017. 98.10% of U.S. and 43.23% of foreign tugboats for sale are direct from Owners. 76 or 18.63% of the tugs worldwide, primarily foreign flagged, were built within the last 10 years, are newbuilding re-sales or currently under construction - compared to 23.37% one year ago and 32.44% five years ago. 71 (17.40%) are over 50 years of age, with six of those over 75 years old. Eleven have no age listed. The oldest tug Marcon currently has listed is a 1940 built 122' LOA, 1,950BHP single screw tug located on the U.S. Great Lakes. This "old lady" is balanced by a 460BHP 47.6' LOA twin screw tug newbuild resale for delivery to Southeast Asia in 2022.

Marcon's Market Comments

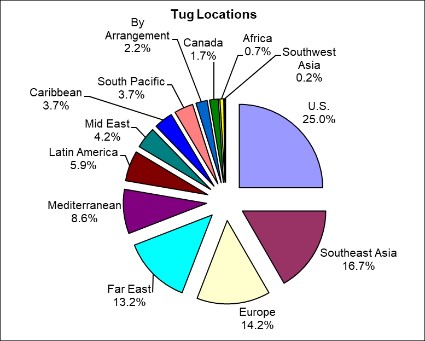

The majority of tugs Marcon tracks for sale as of this report are in the US with 102 tugs officially on the market (vs. 117 one year ago), followed by 68 in Southeast Asia (80), 58 in Europe (54), 54 in the Far East (58), 35 in the Mediterranean (58), 24 in Latin America (33), 17 in the Mid East (31), Caribbean and South Pacific with 15 each (9 and 15, respectively), 9 where location unstated (10), 7 in Canada (6), 3 in Africa (4) and 1 in Southwest Asia (0). Where machinery is known, CAT diesels power 108 or 27% of the tugs listed for sale. This is followed by 58 vessels with EMDs, 46 Niigata, 43 Cummins, 36 Yanmar, 11 Mitsubishi and 10 with Deutz. 90 tugs are powered by other machinery from Akasaka to Wartsila with one Fairbanks Morse tug on the market.

The majority of tugs Marcon tracks for sale as of this report are in the US with 102 tugs officially on the market (vs. 117 one year ago), followed by 68 in Southeast Asia (80), 58 in Europe (54), 54 in the Far East (58), 35 in the Mediterranean (58), 24 in Latin America (33), 17 in the Mid East (31), Caribbean and South Pacific with 15 each (9 and 15, respectively), 9 where location unstated (10), 7 in Canada (6), 3 in Africa (4) and 1 in Southwest Asia (0). Where machinery is known, CAT diesels power 108 or 27% of the tugs listed for sale. This is followed by 58 vessels with EMDs, 46 Niigata, 43 Cummins, 36 Yanmar, 11 Mitsubishi and 10 with Deutz. 90 tugs are powered by other machinery from Akasaka to Wartsila with one Fairbanks Morse tug on the market.

Five years ago, 32.44% of tugs for sale worldwide, primarily foreign flag, were built within the previous 10 years compared to 18.63% today. Then 11.81% of the tugs on the market were 50+ years old compared to 17.40% today. At that time, Marcon had five tugs older than 75 years compared to six today. The average age of all tugs that Marcon has for sale worldwide today is 29 years, with 1993 average build date, compared to 26 years, 1991 average built, in November 2017. The U.S. had the largest selection of tugs listed in 2017 with 164 available (25.8%), followed by 126 in Southeast Asia (19.8%), 70 in Europe (11.0%), 61 in the Mid East (9.6%), Far East 53 (8.3%), Mediterranean 46 (7.2%), 33 in Latin America (5.2%), 20 in the South Pacific (3.1%), 18 Africa (2.8%), 17 Canada (2.4%), 15 in the Caribbean (2.4%), 10 where location is unknown (1.6%) and 2 in Southwest Asia (0.3%).

Five years ago, 32.44% of tugs for sale worldwide, primarily foreign flag, were built within the previous 10 years compared to 18.63% today. Then 11.81% of the tugs on the market were 50+ years old compared to 17.40% today. At that time, Marcon had five tugs older than 75 years compared to six today. The average age of all tugs that Marcon has for sale worldwide today is 29 years, with 1993 average build date, compared to 26 years, 1991 average built, in November 2017. The U.S. had the largest selection of tugs listed in 2017 with 164 available (25.8%), followed by 126 in Southeast Asia (19.8%), 70 in Europe (11.0%), 61 in the Mid East (9.6%), Far East 53 (8.3%), Mediterranean 46 (7.2%), 33 in Latin America (5.2%), 20 in the South Pacific (3.1%), 18 Africa (2.8%), 17 Canada (2.4%), 15 in the Caribbean (2.4%), 10 where location is unknown (1.6%) and 2 in Southwest Asia (0.3%).

Looking at tugs for sale worldwide, conventional twin screw tugs lead with 256 (62.7%) available, followed by 96 azimuthing (23.5%), 37 single-screw (9.1%), 12 Voith Schneider tractors (2.9%) and 7 triple screw (1.7%). This is fairly comparable to five years ago when 14.3% of the 635 tugs for sale were single screw, 58.4% twin screw, 23.1% azimuthing, 3.5% VS tractor and 0.6% triple screw tugs. Bearing in mind that we are focusing on those available for sale, it seems that for the past five years, azimuthing and conventional twin screw tugs have maintained steady positions in the market. Single screw tugs are mostly relegated to nearly zero commercial work, except in certain specific cases. Available for sale units have dropped considerably with many of those being scrapped due to age and condition. It is noted that in November 2022, Sea-Web reported 2,182 tugs worldwide scuttled, broken up or to be broken up world-wide. This is up 4.05% from November 2021's 2,097. Scrapped vessels increased 34.60% between November 2020 and November 2021, after averaging 2% from 2018 to 2019 and then 2019 to 2020. With the decrease in rate of scrapping, it seems that many companies have finished a concentrated effort to scrap its excess tonnage during the worst of the economic fallout of the pandemic. In certain areas of the market, we have seen an increase in demand for tugs and barges, with there being a shortage of units with desired specifications.

Marcon's database shows 227 fewer tugs officially for sale than five years ago in November 2017 with largest shifts in the lower horsepower categories. There are 60 fewer tugs are today listed in the 3-4,000HP range with average age increasing from 24 to 28 years. The 2-3,000HP range lost 56 tugs while their average age increased from 29 to 34 years. The 4-5,000HP range decreased by 42 tugs with average age rising from 19 to 21 years. 32 fewer tugs are listed in the 1-2,000HP range, with average age increasing from 29 to 34 years old. There are 24 fewer 5-6,000HP tugs with average age increasing from 16 to 23 years now. The under 1,000HP tugs category decreased by 10 with a ten year decrease in age to 35 years. There were minor changes in the higher horsepower ranges as far as number available for sale and average age. In summary, we saw a 35.75% drop in listings with a three year increase in overall average age.

Marcon has closed 18 sales and one charter to date in 2022 and we have several additional sales pending at year end and in the first quarter of 2023. These sales included five tugs including 3,000BHP and 3,900BHP twin screw ocean towing tugs; and 1,300BHP and 2,800BHP coastal / ocean twin screw tugs with Marcon acting as sole broker in each transaction. All of these tugs were active and working within the US Registry, and each vessel was certified with a USCG COI Sub "M" certification. The fifth tug sold was a small line handling tug in the Caribbean during the first few months of 2022. Marcon also concluded the sale of a 5,000BHP AHTS between US operators.

The US market for tugs has continued to tighten, and it's been nearly impossible to develop any Azimuthing style tugs in the USA. Owners appear to be keen on continuing to maintain their operating units, with upgrades for machinery as needed when Tier rating requirements are required or upgraded, such as with CARB - California Air Resource Board. This year the CARB has totally phased out Tier 1 tugs from operating in California waters, and at the end of 2023 Tier 2 rated machinery will also be phased out. Tier 3 will be required from January 2024 and is supposed to be good (if it isn't changed by CARB) until December 2027. In certain situations where Tier ratings are required on specific projects and Owner will seek out a Tier 2 rated tug (such as the Houston Ship Canal dredging), or when it's time to retire an older engine and improve fuel consumption. Owners must still often wait months to obtain machinery, even for overhauls and general repairs, due to continued supply chain disruptions, and this will continue into 2023.

Newbuilding costs continue to rise, and the largest component coming out of the US shipyards are Azimuthing ship assist / escort tugs. Shipyards are busy, however, as it doesn't look like the cost increases will reverse itself moving forward. Looking back: between 2000 and 2010 newbuild costs for tugs in the USA effectively doubled. By the end of 2020, that price had doubled again. As noted in an earlier report in 2022, newbuilding costs in US yards jumped some 50-60% between Nov. 2021 and June 2022, and delivery timing delays also continue as everyone must wait for the required parts and machinery to be delivered. Speaking with one Owner earlier in the month he had undertaken the rebuild of a pair of Z-drives. One gear was questionable, and it was decided to replace this one item as part of the rebuild. No problem, as long as you have six months to wait for delivery of this one part.

Commercial Marine Brokers since 1981