Offshore Support Market Report - Sept 2021

Of the 13,598 vessels and 3,712 barges Marcon tracks as of end-September 2021, 2,953 are supply and tug supply boats, with 359 officially on the market for sale. 69.37% of foreign and 70.07% of U.S. flag supply / tug supply boats Marcon has officially listed for sale are directly from Owners. In addition to those for sale, Marcon has 119 straight supply and tug supply vessels listed for charter worldwide, but there are many more in today's market idle and hungry for employment.

1,156 of the vessels tracked by Marcon are crew, fast supply & pilot boats with 228 officially on the market for sale, plus 42 boats are available for charter worldwide. 39.0% of the boats officially for sale are U.S. flag. 63 crew boats for sale worldwide were built within the last 10 years. 64 boats, or 28.07%, are 25 years of age or older. The oldest boat listed is a 40', 240BHP 1957 built and located U.S. Northwest. This vessel is counterbalanced by eight foreign 2020 built 45.9' to 127.9' LOA crew boats, six of which are located in the Mediterranean, one in the Far East and the other in Southeast Asia.

Market Overview

Tug supply boats officially on the market for sale in total is 141, ten fewer than one year ago, September 2020 but the same as five years ago, August 2016. Composition in the last year has changed with the biggest shifts being eight more 12,000-plus HP, seven fewer 10-12,000HP, five fewer 8-9,000HP and three fewer 5-6,000HP AHTSs offered. August 2016, the average age of all AHTSs for sale was 22 years old, where U.S.-flag vessels averaged 31 years and foreign-flag AHTSs averaged 21 years. Today, the average age is 15 years old, with U.S.-flag AHTSs averaging 23 years and foreign-flag averaging 14 years old. At the time of this report, 48 tug supply boats officially for sale were either built within the last 10 years or are newbuilding re-sales. Only 9.93% of tug supply boats are 25 years of age. One 5,150BHP and one 12,240BHP newbuilding AHTS resales were scheduled for delivery in 2020. Five years ago, 33.33% of AHTSs for sale were at least 25 years old; while one year ago, 9.93% were at least 25 years old, which is the same as today's 9.33%; the dramatic drop from 2016 to 2020 reflects the purging of older units from the fleets that has slowed down over the past year. At September 2021, the oldest AHTS available from Marcon was built in 1971.

Tug supply boats officially on the market for sale in total is 141, ten fewer than one year ago, September 2020 but the same as five years ago, August 2016. Composition in the last year has changed with the biggest shifts being eight more 12,000-plus HP, seven fewer 10-12,000HP, five fewer 8-9,000HP and three fewer 5-6,000HP AHTSs offered. August 2016, the average age of all AHTSs for sale was 22 years old, where U.S.-flag vessels averaged 31 years and foreign-flag AHTSs averaged 21 years. Today, the average age is 15 years old, with U.S.-flag AHTSs averaging 23 years and foreign-flag averaging 14 years old. At the time of this report, 48 tug supply boats officially for sale were either built within the last 10 years or are newbuilding re-sales. Only 9.93% of tug supply boats are 25 years of age. One 5,150BHP and one 12,240BHP newbuilding AHTS resales were scheduled for delivery in 2020. Five years ago, 33.33% of AHTSs for sale were at least 25 years old; while one year ago, 9.93% were at least 25 years old, which is the same as today's 9.33%; the dramatic drop from 2016 to 2020 reflects the purging of older units from the fleets that has slowed down over the past year. At September 2021, the oldest AHTS available from Marcon was built in 1971.

Compared to one year ago, we have 17 more PSVs listed for sale. The greatest changes in the vessel size composition are seven more 200'-220' with an average age of 17 years vs 15, seven more 220'-240' (21 years old vs 20 years old), five more over 240' (13 years vs 12 years), three more 150'-160' (20 vs 20 years) and three fewer 190'-200' (23 vs 21 years) PSVs presently on the market. Similar to the anchor handling tug supply boats, PSVs now being offered are generally younger than those offered back in August 2016 with the average age of all available for sale decreasing from 22 years of age to 19 years old now. As of this report, Marcon officially has available 40 supply boats built within the last ten years, which includes two 213', 4,000BHP newbuilding re-sales which were scheduled for delivery in 2020 in the Far East. 39 PSVs, or 17.89%, are 25 years of age or older, with the oldest PSV listed built in 1971 - compared to one year ago when 43 PSVs (21.39%) were older than 25 years with the oldest a 1971-built PSV. Five years ago, the oldest PSV on the market for sale was built in 1964, but 38 PSVs (30.16%) were older than 25 years.

Compared to one year ago, we have 17 more PSVs listed for sale. The greatest changes in the vessel size composition are seven more 200'-220' with an average age of 17 years vs 15, seven more 220'-240' (21 years old vs 20 years old), five more over 240' (13 years vs 12 years), three more 150'-160' (20 vs 20 years) and three fewer 190'-200' (23 vs 21 years) PSVs presently on the market. Similar to the anchor handling tug supply boats, PSVs now being offered are generally younger than those offered back in August 2016 with the average age of all available for sale decreasing from 22 years of age to 19 years old now. As of this report, Marcon officially has available 40 supply boats built within the last ten years, which includes two 213', 4,000BHP newbuilding re-sales which were scheduled for delivery in 2020 in the Far East. 39 PSVs, or 17.89%, are 25 years of age or older, with the oldest PSV listed built in 1971 - compared to one year ago when 43 PSVs (21.39%) were older than 25 years with the oldest a 1971-built PSV. Five years ago, the oldest PSV on the market for sale was built in 1964, but 38 PSVs (30.16%) were older than 25 years.

In today's market many additional vessels, probably equal to or greater than the number "officially" listed can be developed on a private & confidential basis â just a phone call or e-mail away. In general, serious buyers can pick up relatively newer vessels now than in the past.

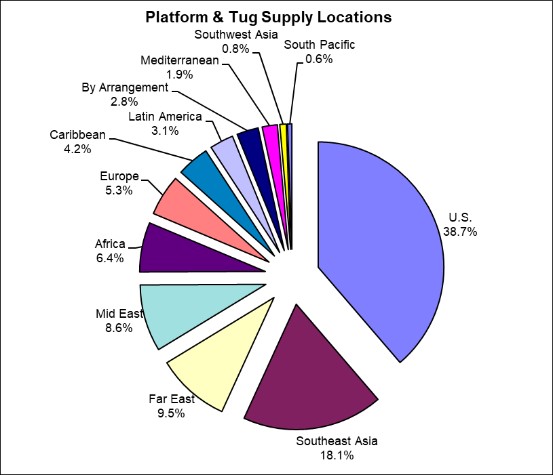

The dominant location for second-hand tonnage on the market September 2021 is the U.S. with 38.7% (up from 38.4% one year ago and 34.1% five years ago) followed by Southeast Asia with 18.1% (up from 17.6% one year ago but down from 22.8% five years ago), Far East with 9.5% (down from 9.9% last year but up from 8.6% in 2016), Mid-East with 8.6% (up from 7.4% last year but down from 12.7% five years ago), Africa with 6.4% (down from 9.7% last year but up from 4.1% in 2016) and Europe with 5.3% (compared to 3.4% last year and 3.7% five years ago). Where location is unknown is 3.1%. The rest of the globe makes up the final 10.6% of locations. CAT is the principal main engine supplier to this sector powering 155 of the supply & tug supply vessels listed for sale, followed by Cummins in 48, 27 each with Bergen and Niigata, Wartsila in 22, 19 with Yanmar, 17 with EMDs and 16 with MAK. 26 units are powered by various other manufacturers. Compared to five years ago, the percentage of available for sale PSVs and AHTSs powered by CATs grew 13%, while those powered by EMDs decreased 9%.

In September 2021 228 crew boats were officially on the market for sale by Marcon, four more than one year ago and 21 more, or 10.14%, than August 2016. Over the last year, composition of LOA ranges has changed with the biggest shifts being five more 110'-120' LOA with an average age of 23 years (vs. same one year ago), four fewer 40'-50' LOA (average age 21 years now and one year ago) and three more each 120'-130' LOA (28 years now and one year ago) and over 130' LOA (18 years vs. 17 years) crew boats offered. As of this report, 27.63% of the crew boats available are less than 10 years old, down from 30.36% reported one year ago and from the 36.23% reported five years ago. In looking at overall fleet age and then by U.S.-flagged versus foreign flagged, over the past five years we can see a slight increase in the age of crew boats on the market. Five years ago, the average age of all on the market through Marcon was 18 years, compared to 20 years one year ago and 21 years as of this report. Older U.S.-flagged vessels remain on the market, consistently was 29 years old for August 2016, September 2020 and now. Foreign flagged crew boats' age increased slightly from 14 years old one and five years ago and is now 15 years, which is about half the age of U.S. vessels. According to IHS Fairplay Sea-web, of crew boats greater than 99GT, 49 are shown as of September 7, 2021 as scuttled, scrapped or to be broken up. This is up four or 8.89% from one year ago. Smaller crew boats are also slowly being scrapped by owners due to lack of work and purchase interest.

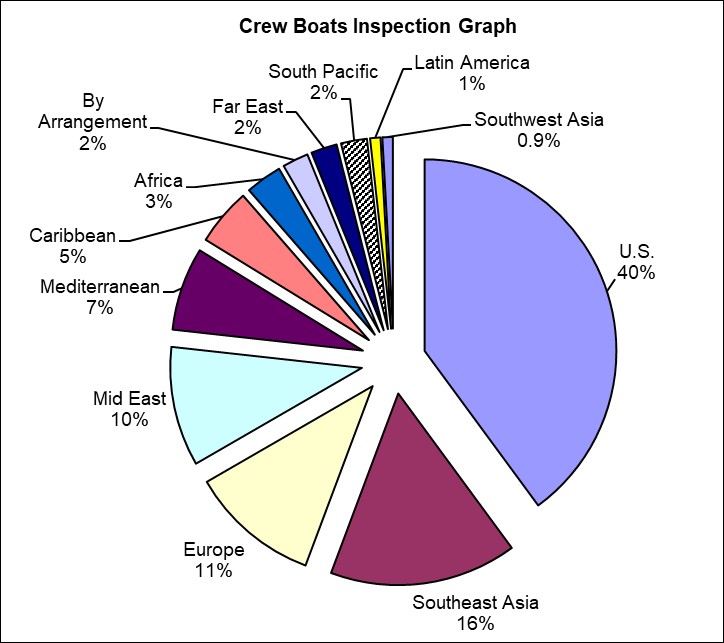

The dominant location for second-hand tonnage on the market September 2021 is the U.S. with 39.9% (down from 42.0% one year ago but up from 34.3% five years ago) followed by Southeast Asia with 15.8% (up from 15.2% one year ago and down from 18.4% five years ago), Europe with 11.0% (up from 10.7% last year but down from 12.1% in 2016), Mid East with 10.1% (up from 9.8% in 2020 and 9.7% in 2016) and Mediterranean with 7.0% (up from 6.7% last year and 4.3% in 2016). Where location is unknown is 2.2%. The rest of the globe makes up the final 14.0% of locations. Of the crew, pilot boats and launches listed, the most popular engine is CAT in 75 of 226 boats where engines are given, followed by 54 Cummins, 53 GM/DD, 12 with MAN-B&W, 9 with MTU, 5 each Iveco and Volvo/Volvo Penta and 13 under other types, ranging from Baudouin to Yanmar. Compared to one and five years ago, as a percentage of vessels available for sale, there was a significant increase in those powered by CATs, offset by a decrease in the number powered by Cummins.

The pandemic severely stalled sales activity from the second quarter of 2020 onward. So far in 2021, we have completed nine sales, primarily under "best offer" conditions, with several in process. Buyers continue to come in well below sellers' desired prices. In 2020, 23.8% of sales were at sellers' asking price, while the remaining sales were at as low as 42.7% of asking. We have seen sellers' pricing adjust downward to what the market is bearing for vessels of their age and condition or at just above scrap levels in order to get the vessel sold. Nine months to date in 2021, six sales were US to US parties, two were US to Caribbean buyer, one was Caribbean to US and the other was between Southeast Asian parties. In 2020, 71.09% of our sales were US seller to US buyer, 12.43% were US seller to foreign buyer and 16.48% were foreign to foreign sales. Vessels were sold into Canada, the Caribbean and Latin America.

Marcon Broker's CommentsSince our last report in March 2021, the offshore supply market appears to continue to improve in most geographic regions. With the continuing battle with varying country and industry responses to the COVID 19 pandemic, economic crises, natural disasters, global supply chain disruptions, et al, there are unequal changes to the offshore supply market. Marcon has had few inquiries for offshore supply vessels and crew boats in the U.S., though we have heard of some sales at just above scrap prices for laid up tonnage. Operators in the Gulf of Mexico report day rates advancing in the last six months, with term rates recently nearly doubling for medium to large DP-2 PSVs. Boats previously fixed at US $8,000 to US $10,000 per day are now fetching US $15,000 to US $20,000 per day on term contracts. Spot rates have moved even higher following hurricane Ida. The USCG is reportedly extending surveys in the GoM due to lack of shipyard capacity due to hurricane damage and the ongoing labor shortage. With operational boats in limited supply, both second hand prices and rates look to keep improving in the near term. In Asian markets, other shipbrokers are reporting an increase in sales and prices are improving, reflecting the demand in those markets. Foreign and U.S. owners with foreign operations reported increased activity, average day rates, utilization rates and active vessels for the second quarter 2021, mainly in the European, Mediterranean and West African markets, but noted other foreign regions improved slightly as well. Owners don't have as many laid up vessels, though some have been laid up so long that they are not viable sales candidates, therefore more suited for scrap.

Since the end of September, Brent crude oil prices have been in the US $80 per barrel and over range, with projections of hitting US $90, if not higher, by year-end. There are multiple reasons behind the price drive up with none of them supporting long-term stability in prices at this point. A key reason is that with the pandemic and multiple major weather events, supply was restricted and now with markets reawakening, demand has increased. Demand for natural gas and oil has increased those prices, which will increase oil demand, especially in Asia.

As of October 15th, U.S. rig counts had increased for the sixth consecutive week with a total of 543, compared to 282 one year ago. However, only 12 of those are in the U.S. Gulf of Mexico, compared to 14 one year ago, the remainder are land-based. However, the 12 units in the US GoM do signal an increase in activity for the region, albeit a slow one.

Governmental interventions are uncertain as far as impact on demand for offshore supply vessels at this time. In the U.S., President Biden is still trying to get a comprehensive infrastructure bill passed with no one quite certain which segments of the maritime industry will be benefited. Globally, the United Nations Climate Change Conference (COP 26) is scheduled to begin 31 October in Glasgow. Given the events of the past two years, resulting from the pandemic and global economic crises, the leading nations are behind in targets for hitting net zero emissions and other climate change goal posts. In fact, increased demand and prices are being noted among fossil fuel types, despite ongoing pressure to convert to renewable energy sources. We have seen a number of offshore supply vessels under go conversions to support windfarms, but this still remains a small part of the market for existing vessels.

Commercial Marine Brokers since 1981