Offshore Market Report - March 2023

Of the 13,370 vessels and 3,747 barges Marcon tracked as of mid-March 2023, 2,937 are supply and tug supply boats, with 245 officially on the market for sale. 64.34% of foreign and 80.39% of U.S. flag supply / tug supply boats Marcon has officially listed for sale are direct from Owners. In addition to those for sale, Marcon has 59 straight supply and tug supply vessels listed for charter worldwide.

1,154 of the vessels tracked by Marcon as of mid-March 2023 are crew, fast supply & pilot boats with 180 officially on the market for sale, plus 48 boats are available for charter worldwide. 40.0% of the boats officially for sale are U.S. flag. 38 crew boats for sale worldwide were built within the last 10 years. 59 boats, or 32.78%, are 25 years of age or older. The oldest boat listed is a 40', 240BHP 1957 built and located U.S. West Coast. This vessel is counterbalanced by a 170.6' LOA foreign 2022 built crew boat in Southeast Asia.

Market Overview

Tug supply boats officially on the market for sale listed with Marcon in total is 77, 79 fewer than March 2022 and 80 fewer than February 2018. Composition in the last year has changed with dropping 83 AHTSs in the 3,000BHP to 9,000BHP and 10,000BHP to 12,000BHP ranges, while gaining seven in the over 12,000BHP category. February 2018, the average age of all AHTSs for sale was 15 years old, where U.S.-flag vessels averaged 26 years and foreign-flag AHTSs averaged 15 years. Today, the average age is 16 years old, with U.S.-flag AHTSs averaging 25 years and foreign-flag averaging 14 years old. At the time of this report, 20 tug supply boats officially for sale were either built within the last 10 years, including four newbuilding re-sales.Only 15.58%, or 12, of tug supply boats are 25 years of age, compared to five years ago, when 19.23% of AHTSs for sale were at least 25 years old; and one year ago, 13.33% were at least 25 years old. At March 2023, the oldest AHTS available from Marcon was built in 1973.

Tug supply boats officially on the market for sale listed with Marcon in total is 77, 79 fewer than March 2022 and 80 fewer than February 2018. Composition in the last year has changed with dropping 83 AHTSs in the 3,000BHP to 9,000BHP and 10,000BHP to 12,000BHP ranges, while gaining seven in the over 12,000BHP category. February 2018, the average age of all AHTSs for sale was 15 years old, where U.S.-flag vessels averaged 26 years and foreign-flag AHTSs averaged 15 years. Today, the average age is 16 years old, with U.S.-flag AHTSs averaging 25 years and foreign-flag averaging 14 years old. At the time of this report, 20 tug supply boats officially for sale were either built within the last 10 years, including four newbuilding re-sales.Only 15.58%, or 12, of tug supply boats are 25 years of age, compared to five years ago, when 19.23% of AHTSs for sale were at least 25 years old; and one year ago, 13.33% were at least 25 years old. At March 2023, the oldest AHTS available from Marcon was built in 1973.

At 168 platform supply vessels listed for sale mid-March 2023, we have 31 fewer PSVs listed for sale compared to one year ago, but three more listed than five years ago. Looking at change in vessel size composition over the past year, the biggest decreases were in the 150' to 160' LOA and over 240' LOA ranges, though there was a fairly consistent decline in all other sizes tracked. PSVs now being offered are slightly newer than those offered back in February 2018 with the average age of all available for sale at 20 years old compared to 22 years old then. U.S.-flagged PSVs decreased from 23 years to 21 years, while foreign flagged decreased from 20 to 17 years old. As of this report, Marcon officially has available 30 supply boats built within the last ten years, with one newbuilding listed. 39 PSVs, or 23.21%, are 25 years of age or older, with the oldest PSV listed built in 1971 - compared to one year ago when 43 PSVs (21.61%) were older than 25 years. Five years ago, 41 PSVs (28.47%) were older than 25 years, but 9 or 6.25% were newbuilds.

At 168 platform supply vessels listed for sale mid-March 2023, we have 31 fewer PSVs listed for sale compared to one year ago, but three more listed than five years ago. Looking at change in vessel size composition over the past year, the biggest decreases were in the 150' to 160' LOA and over 240' LOA ranges, though there was a fairly consistent decline in all other sizes tracked. PSVs now being offered are slightly newer than those offered back in February 2018 with the average age of all available for sale at 20 years old compared to 22 years old then. U.S.-flagged PSVs decreased from 23 years to 21 years, while foreign flagged decreased from 20 to 17 years old. As of this report, Marcon officially has available 30 supply boats built within the last ten years, with one newbuilding listed. 39 PSVs, or 23.21%, are 25 years of age or older, with the oldest PSV listed built in 1971 - compared to one year ago when 43 PSVs (21.61%) were older than 25 years. Five years ago, 41 PSVs (28.47%) were older than 25 years, but 9 or 6.25% were newbuilds.

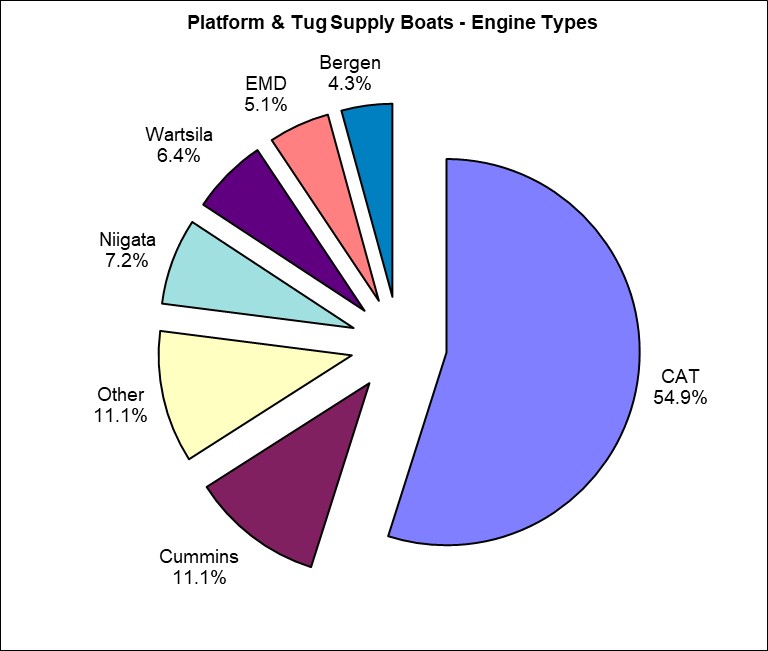

The dominant location for second-hand tonnage on the market March 2023 is the U.S. with 46.8% (up from 43.1% one year ago and 31.2% five years ago) followed by Southeast Asia with 14.3% (down from 17.1% one year ago and from 23.1% five years ago), Far East with 12.7% (compared to 9.2% last year and 12.8% in 2018), Mid-East with 7.6% (8.2% in 2022 and 12.8% in 2018), Caribbean and Europe with 3.9% each (compared to 3.0% and 4.6% one year ago and 4.0% and 2.5% five years ago, respectively) and Africa 3.0% (down from 5.3% last year and 6.9% in 2018). Where location is unknown is 3.0%. The rest of the globe makes up the final 5.1% of locations. CAT is the principal main engine supplier to this sector powering 129 (54.9%) of the supply & tug supply vessels listed for sale, followed by Cummins in 26 (11.1%), 17 (7.2%) with Niigata, 15 (6.4%) with Wartsila, 12 with EMD (5.1%) and 10 with Bergen (4.3%). 26 (11.1%) units are powered by various other manufacturers. Compared to five years ago, the percentage of available for sale PSVs and AHTSs powered by CATs increased by 20.6 percentage points, while those powered by EMD dropped by 4.2 percentage points, Wartsila decreased 2.7 percentage points and Cummins fell 1.4 percentage points.

Crew boats officially on the market now are down 45 and 34 from one year and five years ago, respectively. In terms of vessel size by LOA available compared to five years ago, we saw the most significant declines in crew boats of 100' â 110' and over 130' LOA. As of this report, 21.11% of the crew boats available are less than 10 years old, down from the 23.56% and 24.30% reported one and five years ago, respectively. Conversely, 32.78% today compared to 31.11% last year and 37.85% five years ago are 25 years or older. Five years ago, the average age of all on the market through Marcon was 23 years, compared to 20 years one year ago and as of this report. Older U.S.-flagged vessels remain on the market, though decreasing in age from 34 years in 2018 to 28 years in 2022 but increasing to 29 now. Foreign flagged crew boats' age remained fairly steady at 16 years one year ago and 18 years five years ago compared to 15 years today, but are still almost half the age of U.S. vessels.

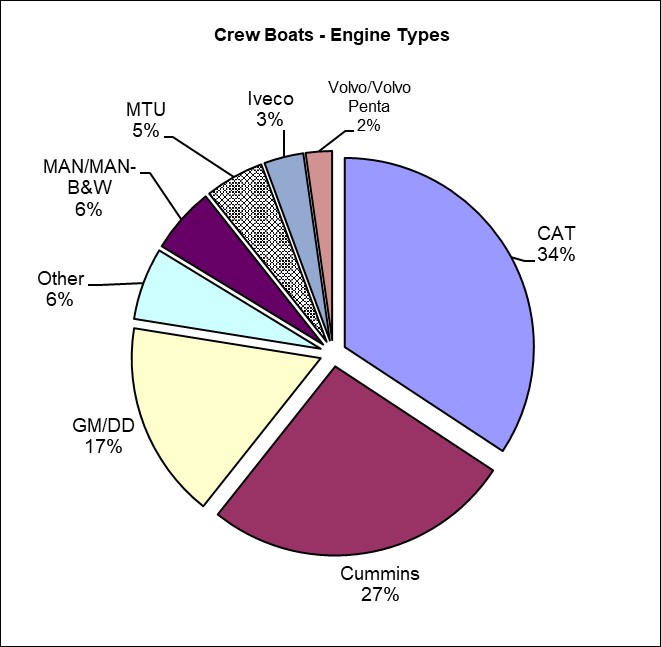

The dominant location for second-hand tonnage on the market March 2023 is the U.S. with 41.1% (up from 37.3% one year ago and 39.3% five years ago) followed by Southeast Asia with 15.0% (down from 16.9% one year ago and up from 14.0% five years ago), Mid East with 12.2% (compared to 10.7% last year and 10.3% February 2018, Europe with 11.1% (versus 10.7% last year and 12.1% five years ago), and the Mediterranean with 7.2% (up from 7.1% last year and 3.7% five years ago). Where location is unknown is 0.6%. The rest of the globe makes up the final 12.8% of locations. Of the crew, pilot boats and launches listed, the most popular engine is CAT in 61 of 180 boats where engines are given, followed by 47 Cummins, 30 GM/DD, MAN-B&W with 10, 9 with MTU, 6 with Iveco, 4 with Volvo/Volvo Penta and 11 under other types, ranging from Baudouin to Yanmar. Compared to one and five years ago, as a percentage of vessels available for sale, there was a significant increase in those powered by CATs and MAN/MAN-B&Ws, offset by decreases in those powered by Cummins and GM/DDs.

The pandemic severely stalled sales activity from the second quarter of 2020 through the end of 2021. In 2021, we completed ten sales, primarily under "best offer" conditions, and one charter. As the world has reopened, we have seen a corresponding increase in demand for tonnage, therefore in 2022, we completed 18 sales and one charter. The 2022 sales and the seven to date in 2023 are at prices reflecting the increased demand, though for some older or rougher condition vessels, we saw prices adjust to what the market would bear. Of our sales to date in 2023, four sales were US to US parties, one was US to Carribean buyer and two were between foreign parties into the Caribbean and South America. In 2022, 13 of our 18 sales were US seller to US buyer, one was US seller to foreign buyer, one was foreign to US buyer and three were foreign to foreign sales. Vessels were sold into the Africa, Canada and Europe.

Marcon Broker's CommentsThe offshore oilfield market has continued to make marked improvement since our last offshore supply market report published in November 2022, and shows no signs of abeyance looking into the future. Rates continue to strengthen and vessel sales into and out of the oilfield market continue to move at a rapid pace. There are recent reports of continuing consolidation, including the March 7th, 2023 Solstad Offshore press release of Tidewater Marine's recent purchase announcement of Solstad's PSV fleet. The purchase includes the entirety of Solstad Offshore's PSV fleet - some 37 - for upwards of US $577 million in cash and new debt on hand. These sort of deals, coupled with continued retirement and disposal of last generation's PSVs will continue to tighten up available vessels in the market and these actions, which have been ongoing for the past several years, will continue to strengthen daily hire rates and utilization rates domestically in the US and worldwide. It's interesting to note that reportedly 14 of the Solstad Offshore vessels were identified as 'battery hybrids', which also shows a continuing direction that the industry leaders are taking in an effort to try and trim greenhouse gas emissions from their fleet's services. Along with alternatively powered vessels, ammonia for one, and even all electric tonnage coming into the markets are also being noted in maritime fleets and intentions worldwide. This should continue to strengthen new technology developments on many fronts. Coupled with renewed and strengthening demand for reliable hydrocarbon sources for post-Covid reopening and emerging economies, and the lack of investment in new sources over the past several years, post 2016 oil price collapse, and earlier demand drops should continue to strengthen demand for tonnage as we move forward through 2023. Hydrocarbon demand production is expected to remain strong for the foreseeable future, despite the opening of new alternative energy markets and expanding production in other sectors.

Marcon was involved in several sales since our last report including a pair of 265' AHTS vessels into alternative services. Marcon was not involved in this sale, but Northstar Marine Inc. of Clermont, New Jersey recently announced the purchase of the 265' AHTS vessel "Northstar Navigator" (ex-Keith Cowan) for continued service in the US Northeast offshore wind farm market, which is really taking hold after years of preparation and stuttered starts. Despite newbuilding announcements for purpose built and dedicated offshore wind service vessels being announced, we expect that these sorts of sale events will continue as there is a dedicated effort for transition to new and alternative energy sources. This will require the combined services of large offshore players to support continued developments in this sector. Along these lines, Fincantieri, through its U.S. subsidiary Fincantieri Marine Group in Sturgeon Bay, Wisconsin announced the newbuild contract for a purpose built Service Operation Vessel (SOV) on January 18, 2023 with CREST Wind, a joint venture between Crowley and ESVAGT. The 288' LOA vessel is expected to go into service in 2026, and is to be dedicated to the Dominion Energy Coastal Virginia Offshore Wind project under long-term charter. The expected increase in offshore wind production capacities in the US will continue to drive major developments as this specific segment comes online and grows, playing catch up with Europe and Asia in this rapidly developing and expanding market. The US Department of Interior announced on February 22, 2023 that it is proposing the first-ever offshore wind lease sale in the Gulf of Mexico. This proposed sale was made in an effort to support the stated goal of increasing offshore wind for the goal of increasing the capacity and deployment of some 30gW of offshore wind energy capacity by 2030. The date of the lease sale has not yet been set, but is reported to include a 102,480-acre area offshore Lake Charles, Louisiana, and two areas offshore Galveston, Texas, one comprising 102,480 acres and the other comprising 96,786 acres.

Commercial Marine Brokers since 1981