Following is a breakdown of pushboats Marcon has available for sale worldwide. Most of these are typical U.S. inland river units, although there are a few foreign pushboats listed from Europe, Latin America and Southeast Asia.

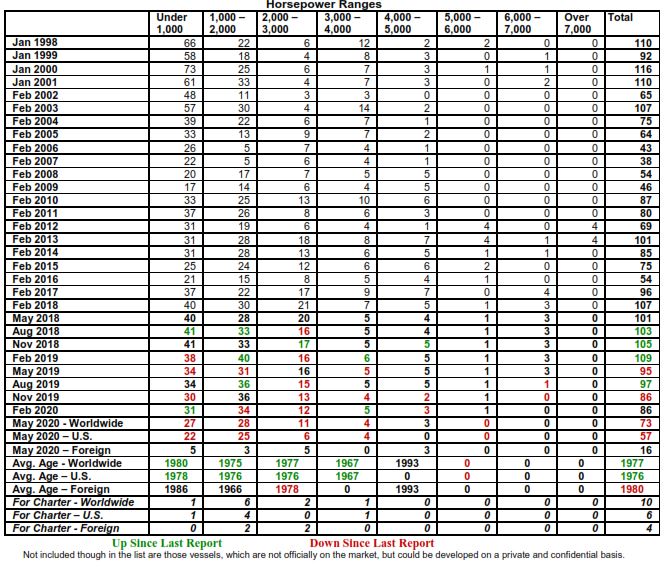

Of the 13,562 vessels (excluding barges) Marcon currently tracks, 779 are inland river pushboats with 73 officially on the market for sale (57 U.S. flag and 16 foreign flag). Seven of the boats with age listed were built within the last ten years. 38 boats are forty-five years of age or older. The oldest listed was built in 1944, a 76', 1,110BHP vessel in the U.S. Northwest. This is counterbalanced by a 2019-built 56', 1,500BHP U.S. flag inland river pushboats located in the U.S. Northwest. Marcon also has 10 inland river pushboats listed for charter - six U.S. and four foreign.

The number of inland river push boats officially on the market for sale in total is 73, down 25, or 25.77%, from our last report published in August 2019. This is 22, or 23.16%, less than one year ago in May 2019 and six or 8.96% more than in May 2015. Composition of horsepower range in the last year has changed with the biggest shifts being seven fewer under 1,000HP with an average age of 1980 (compared to 1970 one year ago), five fewer 2,000-3,000HP (average age now 1977 vs. 1973 one year ago) and three fewer 1,000-2,000HP (1975 vs. 1972) push boats offered. Today, we do not have any push boats offered greater than 5,000HP, reflecting that higher horsepower units are working consistently despite the current events. For now, only 9.59% of the push boats available are less than 10 years old, up from the 7.37% reported one year ago and from the 7.46% reported five years ago. In looking at overall fleet age and then by U.S.-flagged versus foreign flagged, over the past five years we can see a decrease in overall age and of U.S.-flagged push boats on the market, while average age of foreign-flagged push boats increased. Five years ago, the average age of all on the market through Marcon was 43 years, compared to 46 years one year ago and 43 years as of this report. That is driven mostly by older U.S.-flagged vessels going on the market, aging from 46 years in 2015 to 49 years in 2019 then down to 44 years now. Foreign flagged push boats went from 34 years old last year and five years ago and then up to 40 years as of this report date.

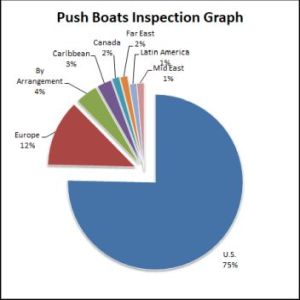

Of the vessels listed for sale, CAT engines are most popular with machinery in 21 vessels. These are followed by 12 each with GM / Detroit Diesels and Cummins, six each with John Deeres and Mitsubishi, four with EMDs and five with other engine types ranging from Akasaka to Niigata, including one Fairbanks Morse. Most of the inland river pushboats Marcon has listed for sale are located in the U.S. with 55 vessels or 75%; followed by nine or 12% in Europe, three with "undisclosed" location, two in the Caribbean and one each in Canada, the Far East, Latin America and the Mid East. As would be expected, this distribution is fairly consistent with one and five years ago, where 81% and 79%, respectively, of pushboats were located in the U.S. Our focus is on the U.S. market, so foreign flagged vessels will naturally be a small portion of our offerings.

Of the vessels listed for sale, CAT engines are most popular with machinery in 21 vessels. These are followed by 12 each with GM / Detroit Diesels and Cummins, six each with John Deeres and Mitsubishi, four with EMDs and five with other engine types ranging from Akasaka to Niigata, including one Fairbanks Morse. Most of the inland river pushboats Marcon has listed for sale are located in the U.S. with 55 vessels or 75%; followed by nine or 12% in Europe, three with "undisclosed" location, two in the Caribbean and one each in Canada, the Far East, Latin America and the Mid East. As would be expected, this distribution is fairly consistent with one and five years ago, where 81% and 79%, respectively, of pushboats were located in the U.S. Our focus is on the U.S. market, so foreign flagged vessels will naturally be a small portion of our offerings.

Actual sale prices of all vessels and barges sold by Marcon so far in 2020 have averaged 94.61% of asking prices, compared to 2019's 89.15% and 2018's 77.79%.

Marcon's Market Comments

Push boats need barges to push. It appears that there are plenty of barges in the market, but whether they need to be pushed anywhere, or not, will have an effect on the demand for tonnage. Currently Marcon does not have any sales of pushers to report, and the sale and purchase market continues to be having a tough ride - at least on the dry cargo side of the market.

During the first quarter of 2020, we saw in the inland river systems of the United States an expected drop in freight activity due to the effects of the Covid-19 shutdowns, decreasing consumer demand domestically and decreased manufacturing output. All of these had a major impact on the entire dry market segment. The record setting flooding during 2019 (292 days lasting from Spring through mid-August was unprecedented), and this 2020 season has started out similar to 2019 causing fears of a repeat of last year's difficulties. High water levels and spring flooding will always have an impact on the market, which also delay plantings, causing reduced demand for fertilizer heading north in the early part of the year. This current season’s sustained high-water conditions have already made it difficult to move cargo and there have been additional delays caused by unplanned closures. Delays to infrastructure projects have also helped to trigger overcapacity, which can be an impetus for consolidation and buyouts. All of this continued downward trending activity will only lead to more idling of equipment and a corresponding fallout of demand.

Seacor Marine's subsidiary SCF barges reports that its fleet continues to move grain on the inland waterways, and its terminals transfer agricultural and industrial essentials. There was a 4 percent year-over-year decline in U.S. grain exports through the Gulf of Mexico, and this reduced demand for barge freight and activity levels at the company's terminals on the Mississippi and Illinois rivers. The company blamed the trade war with China, U.S. farm subsidy programs that were a disincentive to exports, and competition from South America in the market.

American Commercial Barge Line filed for Chapter 11 bankruptcy in February 2020 citing debt and an oversupply of barges in the market. The fleet is always in need of renewal, but overbuilding during the last several years, in the hopes of continued high volumes of cargo demand, mainly from China, were dashed over the past few years, and this has had the effect of placing too much barge tonnage into the market. Accelerated depreciation of assets also encouraged building of new tonnage that may, or may not have actually had a real use at the time. CEO and President Mark Knoy advised that their pre-packaged restructuring plan would reduce the company's debt by nearly US $1 billion, and it is hoped that this will make ACBL stronger in the long run. The company, which is also the former parent company of JeffBoat (which closed its barge building shipyard in Jeffersonville, IN in 2018) re-remerged from this bankruptcy at the end of April 2020 with $200 million in new equity capital.

It is generally considered at this time that the dry cargo market is about 20% over supplied with barges and an expected weakened demand can continue to be foreseen related to trade disputes and other factors moving forward during 2020. China's total imports of soy beans have dropped upwards of 12% (April 2020 report), and this was attributed to bad weather and delaying of cargoes (which are now majority supplied by Brazil). However, this all comes on the heels of a total collapse in the market in 2018 due mainly to a trade war with China. This literally killed overall demand in the Far East exports, and leveled a 75% drop in demand from that reliable Buyer of the product during that year. The drop in overall coal demand, agriculture related planting delays and the drop in demand for cargoes like sand (fracking industry shut down due to collapse of oil prices in the quarter), are contributing to the collapse in demand for tonnage creating an 'over tonnage' situation for the inland market. Overall export levels to the Far East market remain stagnant, and a continued re-brewing of a new trade war with China (attributed to fallout over the Covid-19 response, as well as actions taken by the nation in Hong Kong), will likely continue to hamper exports in the bulk grain markets for an unknown, but extended, period of time.

Commercial Marine Brokers since 1981