Offshore Support Market Report - March 2021

Of the 13,595 vessels and 3,691 barges Marcon tracks as of mid-March 2021, 2,965 are supply and tug supply boats, with 381 officially on the market for sale. 68.29% of foreign and 72.59% of U.S. flag supply / tug supply boats Marcon has officially listed for sale are directly from Owners. In addition to those for sale, Marcon has 116 straight supply and tug supply vessels listed for charter worldwide, but there are many more in today's market idle and hungry for employment.

1,154 of the vessels tracked by Marcon are crew, fast supply & pilot boats with 237 officially on the market for sale, plus 39 boats are available for charter worldwide. 43.0% of the boats officially for sale are U.S. flag. 60 crew boats for sale worldwide were built within the last 10 years. 72 boats, or 30.38%, are 25 years of age or older. The oldest boat listed is a 51', 460BHP 1961 built and located U.S. West Coast. This vessel is counterbalanced by seven foreign 2020 built 45.9' to 90.6' LOA crew boats, six of which are located in the Mediterranean and the other in the Far East.

Market Overview

Tug supply boats officially on the market for sale in total is 158, 12 more than one year ago, March 2020 and 17 more than five years ago, February 2016. Composition in the last year has changed with the biggest shifts being 17 more 12,000-plus HP, three more 8-9,000HP, three more 9-10,000HP and three fewer 7-8,000HP AHTSs offered. In today's market many additional vessels, probably equal to or greater than the number "officially" listed can be developed on a private & confidential basis - just a phone call or e-mail away. In general, serious buyers can pick up relatively newer vessels now than in the past. February 2016, the average age of all AHTSs for sale was 17 years old, where U.S.-flag vessels averaged 29 years and foreign-flag AHTSs averaged 17 year. Today, the average age is 15 years old, with U.S.-flag AHTSs averaging 25 years and foreign-flag averaging 14 years old. At the time of this report, 41 tug supply boats officially for sale were either built within the last 10 years or are newbuilding re-sales. Only 10.13% of tug supply boats are 25 years of age. One 5,150BHP and one 12,240BHP newbuilding AHTS resales were scheduled for delivery in 2020. Five years ago, 32.62% of AHTSs for sale were at least 25 years old; one year ago, 12.33% were at least 25 years old; both more than today's 10.13%, reflecting the purging of older units from the fleets over the past five years. At March 2021, the oldest AHTS available from Marcon was built in 1971.

Tug supply boats officially on the market for sale in total is 158, 12 more than one year ago, March 2020 and 17 more than five years ago, February 2016. Composition in the last year has changed with the biggest shifts being 17 more 12,000-plus HP, three more 8-9,000HP, three more 9-10,000HP and three fewer 7-8,000HP AHTSs offered. In today's market many additional vessels, probably equal to or greater than the number "officially" listed can be developed on a private & confidential basis - just a phone call or e-mail away. In general, serious buyers can pick up relatively newer vessels now than in the past. February 2016, the average age of all AHTSs for sale was 17 years old, where U.S.-flag vessels averaged 29 years and foreign-flag AHTSs averaged 17 year. Today, the average age is 15 years old, with U.S.-flag AHTSs averaging 25 years and foreign-flag averaging 14 years old. At the time of this report, 41 tug supply boats officially for sale were either built within the last 10 years or are newbuilding re-sales. Only 10.13% of tug supply boats are 25 years of age. One 5,150BHP and one 12,240BHP newbuilding AHTS resales were scheduled for delivery in 2020. Five years ago, 32.62% of AHTSs for sale were at least 25 years old; one year ago, 12.33% were at least 25 years old; both more than today's 10.13%, reflecting the purging of older units from the fleets over the past five years. At March 2021, the oldest AHTS available from Marcon was built in 1971.

Compared to one year ago, we have 77 more PSVs listed for sale. The greatest changes in the vessel size composition are 30 more over 240' with an average age of 14 years vs 13, 18 more 200'-220' (16 years old vs 17 years old), 14 more 220'-240' (21 years vs 22 years), seven more 150'-160' (20 vs 21 years) and six each more under 150' (29 years vs 30 years) and 180'-190' (24 vs 33 years) PSVs presently on the market. Unlike the anchor handling tug supply boats, PSVs now being offered are generally older than those offered back in February 2016 with the average age of all available for sale increasing from 17 years of age to 19 years old now. As of this report, Marcon officially has available 35 supply boats built within the last ten years, which includes two 213', 4,000BHP newbuilding re-sales which were scheduled for delivery in 2020 in the Far East. 43 PSVs, or 19.28%, are 25 years of age or older, with the oldest PSV listed built in 1971 - compared to one year ago when 42 PSVs (28.77%) were older than 25 years with the oldest a 1971-built PSV. Five years ago, the two oldest PSVs on the market for sale were built in 1969, but 44 PSVs (33.59%) were older than 25 years.

Compared to one year ago, we have 77 more PSVs listed for sale. The greatest changes in the vessel size composition are 30 more over 240' with an average age of 14 years vs 13, 18 more 200'-220' (16 years old vs 17 years old), 14 more 220'-240' (21 years vs 22 years), seven more 150'-160' (20 vs 21 years) and six each more under 150' (29 years vs 30 years) and 180'-190' (24 vs 33 years) PSVs presently on the market. Unlike the anchor handling tug supply boats, PSVs now being offered are generally older than those offered back in February 2016 with the average age of all available for sale increasing from 17 years of age to 19 years old now. As of this report, Marcon officially has available 35 supply boats built within the last ten years, which includes two 213', 4,000BHP newbuilding re-sales which were scheduled for delivery in 2020 in the Far East. 43 PSVs, or 19.28%, are 25 years of age or older, with the oldest PSV listed built in 1971 - compared to one year ago when 42 PSVs (28.77%) were older than 25 years with the oldest a 1971-built PSV. Five years ago, the two oldest PSVs on the market for sale were built in 1969, but 44 PSVs (33.59%) were older than 25 years.

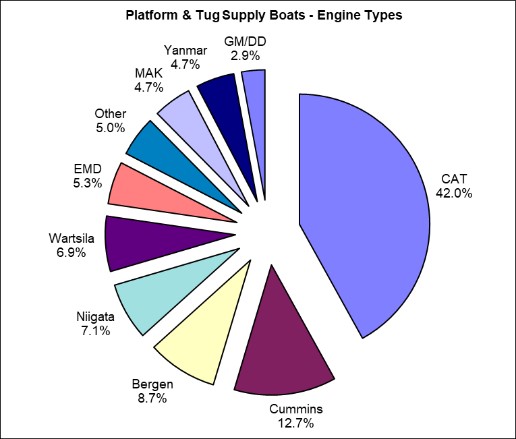

The dominant location for second-hand tonnage on the market March 2021 is the U.S. with 38.3% (up from 33.6% one year ago and 26.1% five years ago) followed by Southeast Asia with 16.0% (down from 19.9% one year ago and 24.3% five years ago), Far East with 8.7% (down from 11.6% last year and 12.5% in 2016), Mid-East with 8.1% (up from 7.5% last year but down from 12.5% in 2016), Europe with 7.9% (up from 5.5% last year and 4.4% five years ago) and Africa with 7.3% (down from 7.5% last year but up from 4.8% in 2016). Where location is unknown is 3.1%. The rest of the globe makes up the final 10.5% of locations. CAT is the principal main engine suppliers to this sector powering 159 of the supply & tug supply vessels listed for sale, followed by Cummins in 48, Bergen in 33, Niigata with 27, Wartsila in 26, 20 with EMDs, 18 each with MAK and Yanmar and 11 with GMs. 19 units are powered by various other manufacturers. Compared to five years ago on a percentage of total basis, CATs, Cummins and Bergen grew while Niigata and EMDs lost positions.

March 2021's number of crew boats officially on the market for sale by Marcon at 237 is up five from one year ago in March 2020 and up 18, or 8.22%, from five years ago in February 2016. Over the last year, composition of LOA ranges has changed with the biggest shifts being seven fewer 40'-50' LOA with an average age of 21 years (vs. 20 years old one year ago), five more 130' and up LOA (average age now 18 vs. 17 one year ago), four more each 60'-70' LOA (25 years old now vs. 31 years old March 2020) and 110'-120' LOA (34 years vs. 31 years) and four fewer 30'-40' LOA (24 years vs. 25 years) crew boats offered. As of this report, 25.32% of the crew boats available are less than 10 years old, up from the 23.28% reported one year ago, but down from the 33.33% reported five years ago. In looking at overall fleet age and then by U.S.-flagged versus foreign flagged, over the past five years we can see an increase in the age of crew boats on the market. Five years ago, the average age of all on the market through Marcon was 18 years, compared to 21 years one year ago and as of this report. Older U.S.-flagged vessels remain on the market, aging from 24 years in 2016 to 30 years in both 2020 and now. Foreign flagged crew boats' age remained steady at 15 years at all three time points, but are still almost half the age of U.S. vessels. According to IHS Fairplay Sea-web, of crew boats greater than 99GT, 47 are shown as of March 11, 2021 as scuttled, scrapped or to be broken up. This is up 15 or 46.88% from one year ago. We have seen this same trend in smaller crew boats as we are told that they were scrapped by owners due to lack of work and purchase interest.

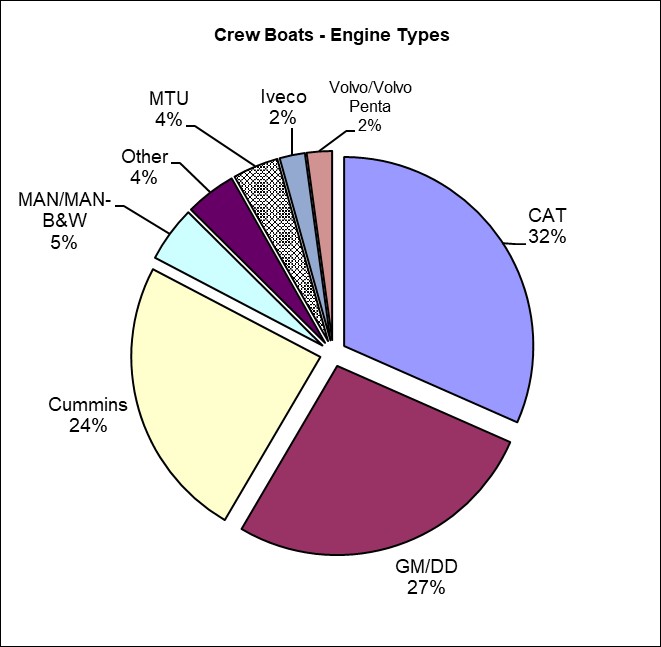

The dominant location for second-hand tonnage on the market March 2021 is the U.S. with 43.9% (up from 40.9% one year ago and up from 34.2% five years ago) followed by Southeast Asia with 14.3% (down from 15.1% one year ago and 17.8% five years ago), Europe with 10.1% (up from 7.8% last year but down from 11.9% in 2016), Mid East with 9.3% (down from 12.1% in 2020 and 10.5% in 2016) and Mediterranean with 6.8% (down from 9.9% last year but up from 4.1% in 2016). Where location is unknown is 1.7%. The rest of the globe makes up the final 13.9% of locations. Of the crew, pilot boats and launches listed, the most popular engine is CAT in 73 of 235 boats where engines are given, followed by 62 GM/DD, 56 Cummins, 11 with MAN-B&W, 9 with MTU, 5 each Iveco and Volvo/Volvo Penta, 4 John Deere and 10 under other types, ranging from Baudouin to Yanmar. Compared to one and five years ago, as a percentage of vessels available for sale, there was a significant increase in those powered by CATs, offset by a decrease in the number powered by Cummins.

The pandemic severely stalled sales activity from the second quarter of 2020 onward. So far in 2021, we have completed three sales, primarily under "best offer" conditions. We are continuing to experience buyers coming in at well below sellers' desired prices. In 2020, 23.8% of sales were at sellers' asking price, while the remaining sales were at as low as 42.7% of asking. This bears out what we've been seeing elsewhere - that sellers' prices have been above what the market is bearing for vessels of their age and condition or at just above scrap levels in order to get the vessel sold. In first quarter 2021, two sales were US to US parties and the other was foreign to foreign parties. In 2020, 71.09% of our sales were US seller to US buyer, 12.43% were US seller to foreign buyer and 16.48% were foreign to foreign sales. Vessels were sold into Canada, the Caribbean and Latin America.

Marcon Broker's CommentsThe market appears to be improving somewhat since we last published any reports. On April 16th, the Baker Hughes Rig count was increased in the US by 7 to 439. This includes land-based rigs (which is at 426) and denotes the obvious shift from offshore to the fracking / tight oil basins (aka Shale) in the USA which has been the case for over a decade with the game changing shale producers making oil and gas production start up to finished product delivered the preference of major investors that. The US Gulf count right now is at 12, and was at 17 one year ago. To give some perspective of how much things have changed, in May of 2001 the offshore rig count in the US Gulf was at 172, and the count has not really held for very long over 100 offshore rigs in the US Gulf since late 2005 / 2006. The last high point was in late December 2014 (just prior to the oil price collapse) when the offshore rig count was at 58 (Dec. 26, 2014). It fell pretty steady after that time and hasn't cracked the barrier of 30 units since Nov. 2015. There were just 12 operating rigs at the end of 2020, and the count has inched back up and down and all are for oil, with zero for gas production for quite some time. The last gas related rig count above zero was in early 2020 (with one and two units operating). This trend is likely to hold, which will still continue to put pressure on the supply of service vessels - even if oil continues to rise - and the availability of supply of oil from sources throughout the world remains very high in relation to the overall demand.

Plugging and abandonment work may be set to improve with the new administration's shift to focus on the backlog of this work, which has been estimated by some sources to be costing some US $104.5 billion worldwide by 2030. If governments become more aggressive on this front, we may see an improvement for service vessels in relation to this service with many of the historically 'new frontier' projects of the 1980s and 1990s coming to the end of their useful service lives. Governments are a fickle source of work, however, with each incoming administration potentially changing course from one direction to the other. Companies would prefer to keep their old rigs producing even a little in order to avoid the abandoning facilities as this is obviously costly, and doesn't bring them any revenue. Regardless, it is projected that oil companies in the US Gulf will be spending about US $1 billion per year for the next 5 years or so to decommission hundreds of wells (source: Woods Mackenzie), so this will keep the service vessel market limping along. However, this is a far cry from the glory days and the OSV / AHTS fleet for the US is still over tonnage with hundreds of vessels continuing to be laid up and many likely never to return to this segment of the industry.

Commercial Marine Brokers since 1981